The Overdue Services Shift

Amidst all the talk of how Canada should respond to Trump and the tariff threat, a few voices have pointed out the importance of services. Stephen Poloz has pointed to some of the data on services and their diversification - something incredibly helpful in light of the dependence on the US for goods exports. Danielle Goldfarb, too, has made the case for the “huge opportunity to sell services to the rest of the world.” Today, I want to look at this topic a bit more and make a case why it is worth more attention.

Canada should be a services powerhouse

While it is certainly better to have access to natural resources rather than be without, too much attention on them can suck up efforts that would be better spent on developing higher-value add parts of the economy. While Canada doesn’t quite fall into the Dutch Disease trap - our economy is more diverse than that - we are still nowhere near as complex or high-value an economy as we should be. That holds back our productivity and prosperity and leaves us vulnerable economically, as Trump is demonstrating.

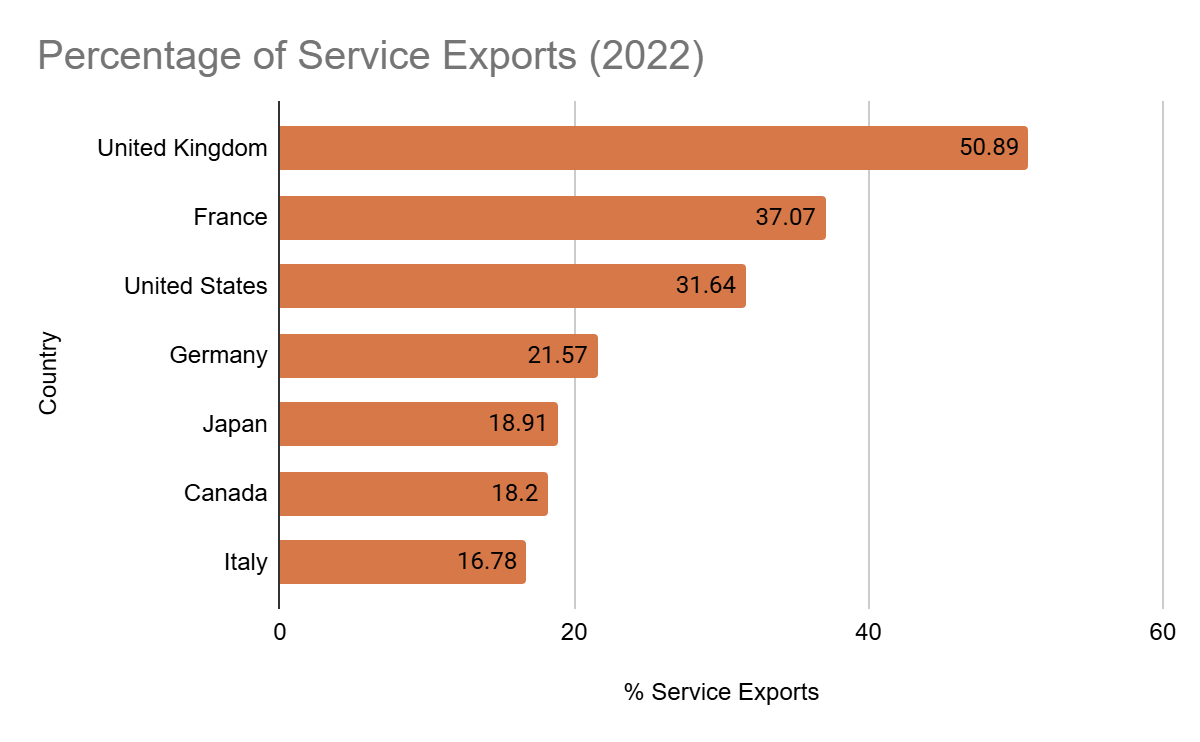

A few data points and analysis sets out where we stand now. First off, we are heavily dependent on goods exports. Out of the G7 countries, we rank second to last in the percentage of exports that are services.

Source: “Canada: Atlas of Economic Complexity”, Harvard Growth Lab, https://atlas.hks.harvard.edu/explore/treemap?exporter

Furthermore, we tend to play in lower parts of the value chain. Research from Global Affairs Canada's Office of the Chief Economist makes that clear:

Canada specializes in the early (upstream) production stages of the supply chain. In general, Canada’s exports will be earlier in the value chain and closer to raw materials, while Canada’s imports will come from later in the value chain and be closer to final goods.

A few notable industries—such as natural resource industries—exemplify Canada’s role as early producers in supply chains. Despite exporting different baskets of goods and services to each trading partner, Canadian exports to all trade partners are, on average, located in the early stages of the supply chain.

Since 1997, Canadian exports have moved to slightly earlier production stages (closer to raw materials) in the value chain, while Canada’s import positioning has stayed relatively constant. The shift in exports to earlier stages occurred in the 2000’s due to a growing share of oil and gas extraction in exports and a diminishing share of auto vehicle manufacturing.

One consequence of that is, not only do we not export as many services as our peer nations, we also don’t embed as many services in those exports. By focusing on upstream production we aren’t utilizing as much R&D, finance, ICT, transportation, or legal services, among others, in the development of our goods.

Our persistantly low R&D intensity is, in part, a reflection of that. You need need relatively little R&D for crude petroleum (economic complexity ranking of -2.56 and 16.37% of our exports), gold (-2.31 and 2.08%) or wood sawn lengthwise (-1.11 and 1.45%) vs serums and vaccines (1.4 and 0.11%) or electronic integrated circuits (1.68 and 0.15%).

Source: Statistics Canada

There are some bright points. Canada’s share of digitally delivered services exports are growing quickly. The most recent data shows that the share of our commercial services exports digitally delivered to customers abroad reached 54% in 2022, up from 39% in 2019, pre-pandemic. This figures part of a wider trend that has seen a rapid growth in services exports, which were up 12.7% in 2023.

This is good, but we need to be working more conciously to grow our services exports, even taking the Trump-factor out of it. As research from the Europea Bank of Reconstruction and Development sets outs, digitally enabled, tradeable services look set to be the key driver of export-led growth.

We need more focus on this space. We have many of the ingredients to be a services powerhouse, not least our diverse and highly educated population. But we still fall short on many fronts, including with through more barriers to services trade than the OECD average. This has to be an area that we give more attention to, fedearlly and provincially, as we seek to strengthen the Canadian economy over the coming months and years.